We, at MB Mortgages always try our best to bring you informative mortgage industry guidelines and knowledge about various products in the financing field. We pride ourselves with our extensive expertise in providing commercial mortgage solutions. We have expertise of commercial real estate capital market, multiple financing options and affordable loan products for any given transaction. We provide financing for commercial real estate and business transactions. Our goal is to keep our clients fully satisfied and happy with our services. In this blog, we will explain and bring knowledgeable information on how the Commercial Mortgages work in Ontario.

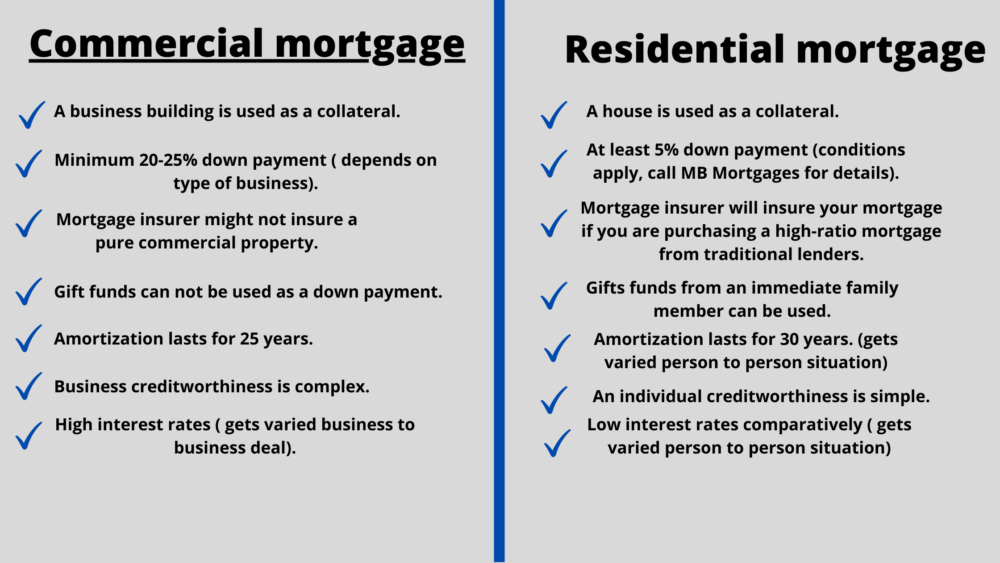

Commercial mortgage works differently than residential mortgages. Commercial mortgage is a loan where business building is used as a collateral and business can be an incorporation, partnership, limited or sole proprietors. Moreover, this loan is riskier than residential mortgage as it depends on how well a business run. On the other hand, a residential mortgage depends on a borrower’s credit history, income and his ability to pay the debts, and evaluation of an individual’ s credit history can be done easily as compare to the evaluation of a business’ credit history.

Also, the riskier the business is, the more complex it becomes to secure a commercial mortgage. The business wanting to secure a commercial mortgage must be financially secure and making a reasonable profit in the long run. Consequently, lenders want more security in the terms of a large down payment, high interest rates, a good credit history and sometimes personal guarantee on a commercial loan. Commercial borrowers also face the risk of going insolvent or bankrupt, and therefore, not eligible to make payments. That is why, lenders might hesitate to approve you for a commercial loan. However, based on your situation, we have a number of options tailored to your needs and can offer you many solutions. Contact MB Mortgages for your commercial mortgage needs.

Here are some frequently asked questions on Commercial mortgage:

1. What is a term for a commercial mortgage?

The term for commercial mortgage ranges from 3-25 years. It depends on what kind of commercial property is being mortgaged.

2. What do you need to do to qualify for a commercial mortgage?

• Debt service coverage ratio- You would need a debt service coverage ratio that means the business income is appropriate to cover all the expenses and debts registered under of it. If the business is running well, apparently, it makes more sense to lender to lend money for commercial mortgage.

• Business credit history- You would need a good business credit history to get approved for a commercial loan, as mortgages want to make sure your business is making payment on time to pay debts, or your business earn enough income to cover all expenses. However, to evaluate a business creditworthiness is complex, which might demotivate mortgagees to lend you money.

• Personal Guarantee on a Commercial Loan – If your business does not have an established credit history of its own, then some lenders require personal guarantee of the owner(s) of the business. A personal guarantee means that the owner(s) will cover the total loan cost if their business cannot pay off its debt, along with any associated legal fees. This is the least risky option for the lender and the most risky one for you as a business owner.

• Recent business situation- You would need how well your business is performing. Lenders want to know if your business income can afford the monthly mortgage payment, property tax, etc. If your business is performing well, it can make lenders to feel safer to lend you money to buy the business premises.

• Minimum down payment 20-25% ( gets varied from business to business situation)- You would need an amount of minimum down payment 20-25%, but in a commercial mortgage, down payment gets varied from business to business, and depends how risky your business is. If your business is risky, you make a large amount of down payment. Unlike residential mortgage, mortgage insurer might not insure a pure commercial premise, but it may insure a mixed residential and commercial building. We at MB Mortgages can guide you through the whole process, also what other documentation you would need to secure a commercial mortgage.

3. What is the difference between commercial mortgage and residential mortgage?

Please contact MB Mortgages to get answers to all your queries. We at MB Mortgages provide commercial mortgage solutions for the following property types:

Property Types-

• Hotels

• Restaurants

• Office Buildings

• Malls / Plazas

• Gas Stations

• Warehouse / Industrial unit

• Retail

• Vacant land

• Golf Courses

• Self Storage

• Special use facilities

Services

• Commercial Mortgages – Purchase / Refinance

• Business Loans

• Equipment Loans

• Business Refinancing

• Truck and Trailer Financing

• Construction Loans

• Line of Credit

Why choose us-

As a leading Mortgage Brokerage, we have strong relations with multiple banks and numerous lenders. We work with Canada’s leading lenders to provide you a mortgage solution that fits your budget. Our mortgage and financing process is amazingly simple, we represent you and match you with the best suited mortgage as per your needs. This way we can guide you through this complicated process with our years of mortgage financing experience.

• We are dedicated and professional Accredited Mortgage Brokers in GTA.

• We are well trained and have experience in the mortgage financing field more than 10 years.

• We can shop around with different lenders to get you the best possible mortgage rates and conditions as well.

• We have different options for different income and credit level with access to number of private lenders to suit borrower’s needs.

Contact us-

We are a professional mortgage broker in GTA. We can help you secure a mortgage with best mortgage interest rates. We are located at 2 County Court Blvd., Suite # 438, Brampton, ON L6W 3W8. Call MB Mortgages Inc. today at 905-458-6929/416-939-7131 for your queries or you can email us at: [email protected] or you can visit our website at www.mbmortgages.ca

The information provided in this blog post is intended to provide general information. You should consult with a mortgage professional to fully determine the scope of your situation. MB Mortgages shall not be held liable from usage of the information provided on this page. Individual situation may vary.