Mostly senior citizens over the age of 55 are often in a situation where they are house-rich but low in cash. They need cash to cover their monthly expenses, renovate the house, pay off high-interest debts. In this situation, a Reverse mortgage comes into play, which helps them access their equity. Today, we would discuss Reverse mortgages in this blog, the pros, and cons, and why you should opt for this. Additionally, we would discuss some frequently asked questions for your better understanding.

What is a reverse mortgage?

A reverse mortgage is an opportunity for older people to access their home equity and receive tax-free cash. They maintain ownership of the home without paying monthly mortgage payments. However, they are required to pay property taxes and any relevant Home insurance.

Reverse mortgage eligibility & qualifications

• A Canadian Homeowner

• Age 55 or older

• Location of the house

• Appraisal value

• Home equity

*For further details, call MB Mortgages Inc. at 905-458-6929/416-939-7131*.

Pros:

• You can receive cash in a one-time lump sum or can receive monthly.

• You can get tax-free cash based on your home equity.

• You can pay your healthcare expenses, high-interest debts or renovate your home.

• You can travel all around the world with your spouse with tax-free cash.

Cons:

• Interest rates are often higher than a regular mortgage.

• As you incur interest on your loan, the equity you hold in your home will go down.

• Your estate must pay the principal loan + accrued interest if you die.

• Reverse mortgage-related costs could be higher than standard mortgages or other credit products.

• You use your equity; consequently, due to high accumulated interest, there might be a low amount of money in your estate to leave to your offspring.

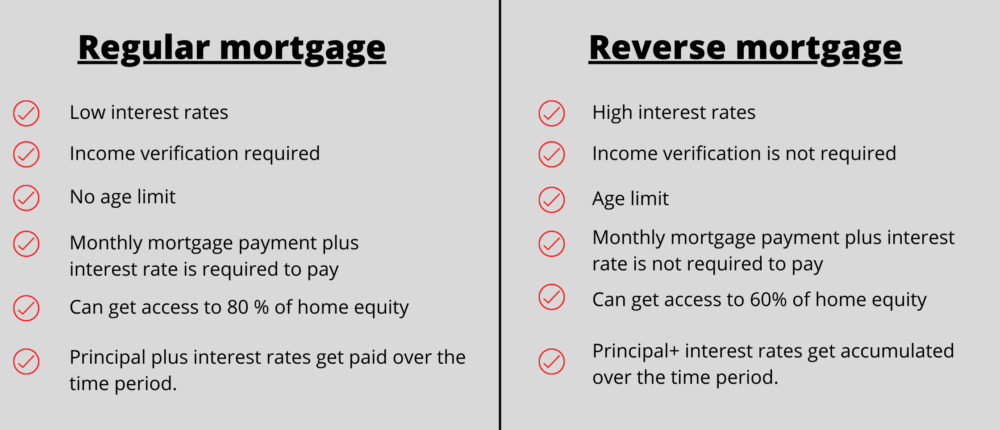

Difference between Regular mortgage and Reverse mortgage:

To reiterate, if you can thoroughly understand this product, you have already discussed it with your immediate family members, mortgage advisor, and you are fully confident to buy it, reverse mortgage can be a good choice to finance towards your retirement. We would like you to opt for it with your conscious mind and after shopping around. You are in safe hands with MB Mortgages Inc., as we have over a decade of experience and always give priority to our client’s choices and needs. Contact us at 905-458-6929/416-939-7131; we can diligently walk you through the process and help you to secure a reverse mortgage.

Here are some frequently asked questions –

1. How much equity is needed to get a Reverse mortgage?

Home equity is calculated from your home’s appraised value by subtracting any outstanding secured loans against the home. The total amount you can borrow must be greater than or equal to any secured debt due on the house. Also, you can get access to 60 % of your home equity.

2. How to get out of a Reverse mortgage?

To pay off a Reverse mortgage, you must pay the principal balance plus accumulated interest over the period. However, you might be asked to pay any fee to pay off a mortgage in advance. You are not required to pay anything except property taxes or Home insurance unless you sell the house.

3. Who pays off deceased’s reverse mortgage?

A lender may usually clarify options for paying off the debt to the borrower’s estate when a reverse mortgage borrower dies. If heirs have enough funds to pay off the loan amount plus accrued interest, they repay it to secure their house. However, in the worst-case scenario, if they lack funds, the Lender might sell the house to pay off the mortgage.

4. What is better than a reverse mortgage?

The traditional mortgage loan such as HELOC to get access to home equity up to 65% Loan to value. You pay less interest rates than reverse mortgage, and your equity amount increases as you pay off the loan amount. On the other hand, in a reverse mortgage, you use your equity, so your estate will have a small sum of cash to leave to your offspring.

5. Is money from a reverse mortgage considered income?

No, reverse mortgage payments are tax-free cash, and they are considered mortgage loan proceeds, not the salary. The mortgagee can pay you either in one lump sum, transfer monthly, and make a line of credit or a combination of three.

6. Can heirs walk away from a reverse mortgage?

The inheritors can walk away, as they are not responsible for paying off the mortgage. In this case, lenders will allow the foreclosure to sell the property to get paid. If the property value is more than the loan amount, heirs will get any amount left from the sale. If the property value is less than the loan amount, they are not bound to pay the extra amount if they walk away from the mortgage.

Why choose us-

As a leading Mortgage Brokerage, we have strong relations with multiple banks and numerous lenders. We work with Canada’s leading lenders to provide you a mortgage solution that fits your budget. Our mortgage and financing process is amazingly simple, we represent you and match you with the best suited mortgage as per your needs. This way we can guide you through this complicated process with our years of mortgage financing experience.

• We are dedicated and professional Accredited Mortgage Brokers in GTA.

• We are well trained and have experience in the mortgage financing field more than 10 years.

• We can shop around with different lenders to get you the best possible mortgage rates and conditions as well.

• We have different options for different income and credit level with access to number of private lenders to suit borrower’s needs.

Contact us-

We are a professional mortgage broker in GTA. We can help you secure a mortgage with best mortgage interest rates. We are located at 2 County Court Blvd., Suite # 438, Brampton, ON L6W 3W8. Call MB Mortgages Inc. today at 905-458-6929/416-939-7131 for your queries or you can email us at: [email protected] or you can visit our website at www.mbmortgages.ca

The information provided in this blog post is intended to provide general information. You should consult with a mortgage professional to fully determine the scope of your situation. MB Mortgages shall not be held liable from usage of the information provided on this page. Individual situation may vary.