If you are looking to get a mortgage and you wonder what a stress test for a mortgage means and requires to qualify, in this blog we will discuss the Mortgage Stress Test in detail and try to answer the most asked queries. Whenever the topic named Mortgage Stress test comes up, buyers think it would be difficult to qualify under these new rules. It can be due to lack of knowledge or they might not consult a knowledgeable broker who can guide them how this test can help you to save more money.

With over a decade of mortgage industry experience, MB Mortgages can help you throughout your financing process in a seamless manner .We can guide you on how this test works, when you need to undergo or if you do not have enough income to pass this test, what options you are left with ? We at MB Mortgages have a bunch of options to help you based on your situation. Please contact us if you have any query based on the stress test mortgage, we offer a no obligation free consultation.

Here are some frequently asked questions on Stress test:

1. What is the mortgage stress test and why was it created?

The new mortgage stress test was created with the intent of protecting both the borrowers and the lenders. Because of the lending interest rate fluctuations and the anticipation of interest rates to go up in the future, the federal government wants to make sure that the borrowers are still able to make payments towards all their debt obligations if the interest rates go up. Or else, if you are not able to afford higher debt obligations in the future, you can end up defaulting on your mortgage and risk losing your home.

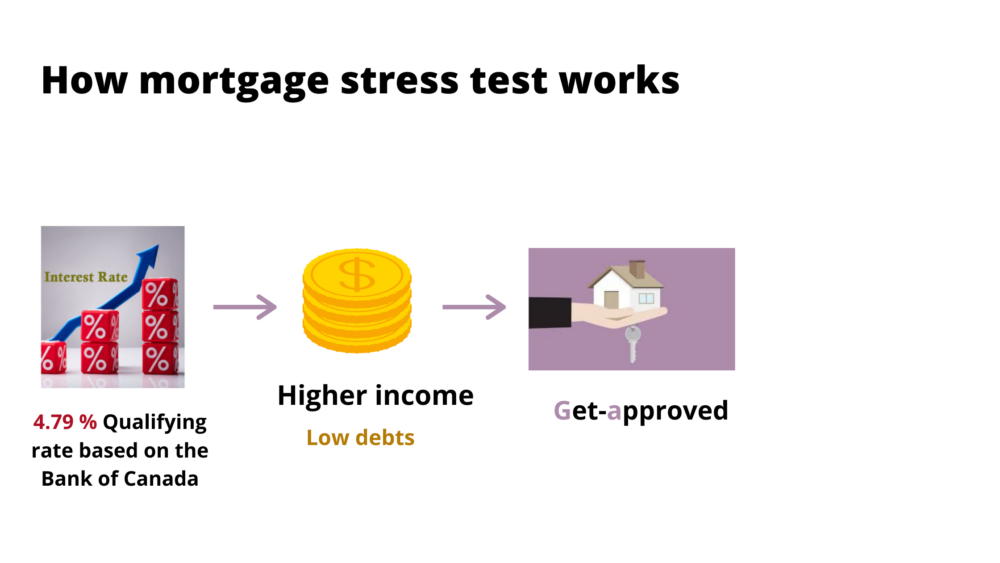

The mortgage stress test requires whether your income can cover all the expenses or not if interest rates spike up in the future. Canadian major banks and all financial institutions( A Lenders) that fall under the Bank of Canada have the same guidelines & they offer competitive interest rates. They must qualify borrowers with 4.79% qualifying rate to check borrower’s affordability if the interest rates go up in the future.

On the other hand, for B lenders, this test considers criteria mortgage interest rate plus 2% or 4.79%, whichever is higher. For example, when you apply for a mortgage with an alternative lenders (B lenders) and they approve you an interest rate of 2.01 %; buyers should know that qualifying rate will not be the same rate as 2.01%. The qualifying rate will be adjusted based on mortgage stress test. Let us say that your mortgage interest rate is 2.01%, then you would qualify on (2.01%+2.00%=4.01% or 4.79% (current qualifying rate), whichever is higher. Based on this example, 4.79% rate is higher, therefore you must qualify at 4.79%.

2. What criteria traditional lenders follow to qualify you under a stress test?

• Firstly, banks consider the GDS (Gross debt service) means that your gross income can cover all the house expenses such as mortgage payment, property taxes, etc. in case if the interest rate surge up in the coming days.

• Secondly, banks consider the TDS (total debt service) to get an idea whether your taxable income can cover all the house expenses plus other debts (car payments, credit card, or any other loan) at a higher rate than you actually would pay. Therefore, Banks consider both GDS & TDS ratios under stress test rules.

• Finally, the buyers can easily qualify under the stress test rules if their credit history is strong.

3. How do stress test mortgage help to save money?

To shed more light, we would like to explain buyers, how they can save money in the long run if they pass the stress test and get mortgage from traditional lenders. Apparently, Canadian major banks offer lower interest rates than Subprime lenders and Private lenders based on income and credit history if buyer pass the stress test. Luckily, some buyers earn good income and therefore they can qualify for lower interest rate. The lower the monthly mortgage payment, the more you save in your pocket.

Why choose us-

As a leading Mortgage Brokerage, we have strong relations with multiple banks and numerous lenders. We work with Canada’s leading lenders to provide you a mortgage solution that fits your budget. Our mortgage and financing process is amazingly simple, we represent you and match you with the best suited mortgage as per your needs. This way we can guide you through this complicated process with our years of mortgage financing experience.

• We are dedicated and professional Accredited Mortgage Brokers in GTA.

• We are well trained and have experience in the mortgage financing field more than 10 years.

• We can shop around with different lenders to get you the best possible mortgage rates and conditions as well.

• We have different options for different income and credit level with access to number of private lenders to suit borrower’s needs.

Contact us-

We are a professional mortgage broker in GTA. We can help you secure a mortgage with best mortgage interest rates. We are located at 2 County Court Blvd., Suite # 438, Brampton, ON L6W 3W8. Call MB Mortgages Inc. today at 905-458-6929/416-939-7131 for your queries or you can email us at: [email protected] or you can visit our website at www.mbmortgages.ca

The information provided in this blog post is intended to provide general information. You should consult with a mortgage professional to fully determine the scope of your situation. MB Mortgages shall not be held liable from usage of the information provided on this page. Individual situation may vary.